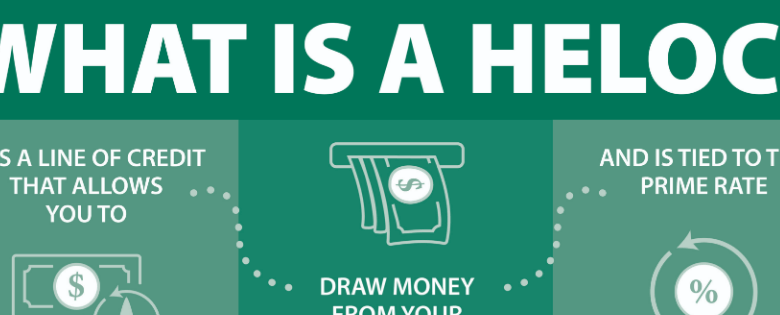

A heloc is a type of loan that allows you to use the equity in your home to cover short-term financial needs. In other words, it’s a quick and easy way to get cash without having to tap into your mortgage or take out a new loan. Here are some things you need to know about heloc requirements if you’re considering borrowing through a heloc: Your credit score matters. The higher your score, the easier it is for you to get approved for a heloc. The interest rates are typically lower than traditional loans. You can use a heloc to bridge a gap until you can solve your current funding problems or reach your long-term financial goals. If you have experience with HELOCs, there are some things you should know before borrowing through one.

What is a heloc loan?

What is heloc loan? A HELOC loan is a short-term, high-interest loan that can be used to bridge a money gap between when you receive income and when you need to pay your bills. A HELOC consists of two parts: the loan amount and the interest rate. The interest rate is continuously variable, so it can change over time.

To get a HELOC loan, you generally need good credit and an acceptable down payment. Your lender will also want to see proof of your income, such as your current paycheck or bank statement. You typically have 30 days to apply for a HELOC, but some lenders may require up to 60 days notice.

The interest on a HELOC Loan compounds daily, so if you don’t pay it off within 30 days it will add another day each week until it’s paid in full. If you miss even one payment on a HELOC Loan, the lender has the right to seize any assets that are in your possession or garnish your wages.

Please note: A HELOC cannot be used as collateral for a bank loan or other type of borrowing product.

What are the requirements for a heloc loan?

If you’re looking for a HELOC loan, there are certain requirements that you must meet in order to qualify. The most important requirement is that your total debt-to-income (TDI) ratio be below 36%. This means that your monthly payments on all your outstanding debt combined cannot exceed 36% of your monthly income.

Additionally, you’ll need to have a good credit score and adequate financial resources available to cover the full amount of the loan. You may also need to provide some documentation verifying your income and debtors. Finally, heloc loans come with interest rates that can be quite high, so it’s important to compare rates before applying.

Why are heloc loans important?

A HELOC loan is an important financial tool that can help you repair or rebuild your home. A HELOC loan is a type of mortgage that allows you to borrow money from a bank or other lending institution, using the equity in your home as security.

HELOC loan has few requirements, compared to traditional mortgages. You don’t need a good credit score, for example, and you won’t need to provide documentation like a down payment. Plus, interest rates are usually lower on HELOCs than on traditional mortgages.

The biggest benefit of a HELOC loan is that it can help you take advantage of low interest rates while you’re repairing or rebuilding your home. This means that you’ll pay less in total interest costs over the life of the loan than if you took out a traditional mortgage.

Another benefit of using a HELOC loan is that it can help protect your equity in your home. If market conditions decline later on in the repayment period, your home may still be worth more than the amount outstanding on your HELOC loan. In this case, you would either be able to sell your home at market value or refinance the debt into a traditional mortgage at a lower rate.

What are the risks of a heloc loan?

There are a few things to keep in mind when considering a heloc loan. First and foremost, the requirements for obtaining a heloc loan vary depending on your state. In most cases, you will need to have good credit, an adequate down payment and meet certain eligibility criteria. Secondly, HELOCs are not always the most appropriate option for everyone. Before taking out a heloc loan, be sure to assess your budget and needs carefully. Finally, remember that HELOCs are subject to interest rates that can be quite high, so make sure you understand the terms of your loan before signing on the dotted line.

Conclusion

Thank you for reading our article on heloc loan requirements. In this article, we provide a brief overview of heloc loan requirements so that you can understand the basics of borrowing money through a HELOC. We also highlight some tips for applying for a HELOC and provide some important information about when you should consider refinance your existing HELOC. Finally, we offer some helpful advice on what to do if you experience financial difficulties with your HELOC. Hopefully, this article has provided you with all the information you need to know to get started with a HELOC loan. If not, be sure to contact one of our advisors at Heloc Loans Online for more assistance!