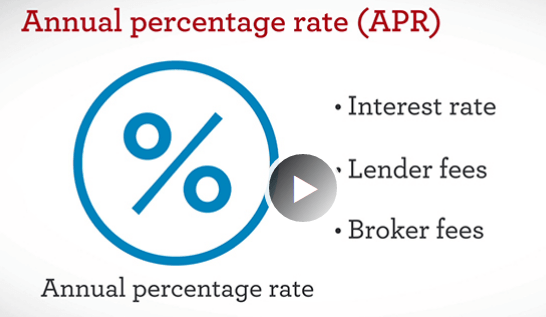

What is apr on a loan? APR is the Annual Percentage Rate that lenders charge for loans. It’s the percentage of interest that you will pay on your loan each year. And it can have a big impact on your borrowing decision. If you’re thinking about taking out a loan. It’s important to understand what APR means and how it can affect you. And if you already have a loan. Be sure to check the APR to see if there has been any increase in recent months.

what is apr on a loan

What is APR on a loan?

An APR is the annual percentage rate that reflects how much interest will be charged on a loan over its lifetime. The APR can be helpful in estimating the cost of borrowing money over time.

What is APR?

APR stands for Annual Percentage Rate. It’s a number that banks and other lenders use to calculate how much you’ll owe on a loan. Based on the interest rate and the amount of time until it’s due. The higher the APR, the higher the interest rate.

Are There Any Fees?

There may be a fee associated with obtaining an APR on a loan. This fee can vary depending on the lender and the loan product.

APR, Loan Terms, and Payment Schedules

The acronym “APR” stands for annual percentage rate. It’s a figure that lenders use to calculate how much you’ll pay on a loan. Based on the amount of the loan and the term of the loan.

Lenders typically offer different APR rates for loans with different terms. For example, you might be offered an APR rate of 4 percent for a 12-month loan. But an APR rate of 10 percent for a 24-month loan.

You also might have to make monthly payments during the term of your loan. Which would affect the APR rate you’re charged. For example, if you have a 12-month loan with an APR of 4 percent and you make six monthly payments of $100 each, your total payments would be $600. Your total interest paid over the life of the loan would be $120 ($600 x .04 = $120), so your overall cost would be lower if you had made one large payment instead of six smaller ones.

Some borrowers opt to borrow money using an installment plan – in which they make smaller payments than regular monthly installments – in order to get low or no interest rates on their loans. This can result in higher monthly payments, though, so it’s important to weigh both factors when deciding whether to borrow money this way.

Conclusion

Apr on a loan conditions can be confusing, but we have put together a comprehensive guide to help you understand APR and what it means for your loan. By learning about APR, you will be able to make an informed decision about whether or not to take out a loan with this information. Keep in mind that the APR you see on loans is just one component of the overall cost of borrowing; other factors include interest rates, fees, and taxes. Use our guide as a starting point to learn more about APR and how it affects your borrowing options.